When multiple parties cause harm to a single victim, courts must decide how to divide legal responsibility. Joint and several liability is the legal doctrine that governs that decision in personal injury cases across the United States. For injured plaintiffs, it can mean the difference between full financial recovery and walking away with nothing.

This guide covers every critical dimension of joint and several liability: its legal definition, how courts apply it, how it interacts with comparative fault, which states still follow it, and real world examples from courtrooms across the country.

Built for plaintiffs, law students, defense attorneys, and anyone who needs a thorough, accurate resource on this foundational area of tort law.

What Is Joint and Several Liability in U.S. Personal Injury Law?

Layperson Explanation

Joint and several liability is a legal rule that holds multiple defendants each fully responsible for the entire amount of damages awarded to a plaintiff, regardless of how much fault each defendant individually contributed to the harm.

If a jury finds three defendants responsible for an injury and awards the plaintiff $900,000, joint and several liability means any one of those defendants can be required to pay the entire $900,000, not just one third of it.

The Legal Definition

In tort law, joint and several liability arises when two or more parties, known as joint tortfeasors, act together or independently to cause a single indivisible injury.

Courts apply the rule to ensure that the plaintiff receives full compensation even when defendants vary in their degree of fault, financial resources, or legal status.

The Core Principle of Shared Liability Law

The doctrine rests on a straightforward rationale: when defendants collectively caused harm that cannot be cleanly divided, the burden of sorting out their respective contributions should fall on them, not on the innocent injured party.

Multiple defendants liability rules like this one shift the risk of insolvent or unavailable co-defendants from the plaintiff to the defendants themselves.

This principle has been part of common law for centuries. Courts in England recognized it in cases involving joint tortfeasors as early as the 1800s, and American courts adopted and refined it throughout the twentieth century as tort litigation became more complex.

How Does Joint and Several Liability Work in Multi Defendant Cases?

Step by Step: From Lawsuit to Recovery

The process through which joint and several liability operates in multi defendant cases follows a clear sequence:

- The plaintiff files a lawsuit naming all parties believed to be responsible for the injury.

- At trial, the jury (or judge in a bench trial) determines which defendants were negligent and assigns a percentage of fault to each.

- The jury calculates total damages, such as medical bills, lost income, and pain and suffering.

- Under joint and several liability, the court enters judgment against all defendants jointly and severally.

- The plaintiff may then collect the full judgment amount from any one defendant or any combination of defendants.

- If one defendant overpays relative to their share of fault, they may seek reimbursement from other defendants through a contribution claim.

The Role of Courts and Juries

Juries do not determine how payments are distributed between defendants. Their job is to find facts: who was negligent, how much each party was at fault, and what total compensation the plaintiff deserves. Courts then apply the applicable liability rule under state law to translate those findings into a judgment.

In states that follow pure joint and several liability, the court does not adjust the judgment based on each defendant’s percentage of fault. The plaintiff holds the full amount against all defendants and pursues collection as they see fit.

A plaintiff may collect the entire judgment from any one defendant. This gives plaintiffs powerful leverage in settlement negotiations and post-judgment collection.

Practical Collection Strategy

Experienced plaintiff attorneys use joint and several liability strategically. If one defendant carries significant liability insurance or has deep financial resources, the plaintiff may focus collection efforts on that party entirely.

The burdened defendant then has the option to pursue other defendants for their share through separate legal proceedings.

Why Can One Defendant Be Forced to Pay 100 Percent of Damages?

The Indivisible Injury Concept

At the heart of joint and several liability is the indivisible injury rule. When multiple defendants cause a harm that cannot be broken down into distinct, measurable portions attributable to each defendant separately, courts treat the injury as a single whole.

Consider a plaintiff who develops a serious respiratory disease after being exposed to toxic chemicals released by three different manufacturers operating in the same industrial zone. Medical science cannot identify what percentage of the disease each manufacturer caused. Because the injury is indivisible, courts refuse to limit any one manufacturer’s responsibility to a fractional share.

This rule protects plaintiffs from uncompensated losses when other defendants cannot pay. Without joint and several liability, a plaintiff with an indivisible injury would bear the financial risk of any defendant’s insolvency, disappearance, or immunity.

Risk Shifting From Plaintiff to Defendants

The practical effect of joint and several liability is a transfer of financial risk. In a world without this doctrine, a plaintiff who recovers a judgment against five defendants and finds that three of them are bankrupt must absorb that shortfall. Joint and several liability reassigns that risk to the remaining solvent defendants.

Courts have consistently justified this risk shift on moral grounds. The defendants created the dangerous situation together. They are in a better position than the plaintiff to manage the consequences of a co-defendant’s insolvency, because they can take steps during the underlying activity to avoid associating with judgment-proof partners, obtain indemnity agreements, or purchase additional insurance.

The Deep Pocket Defendant Rule

Critics sometimes describe joint and several liability as the deep pocket defendant rule because it effectively allows plaintiffs to target whichever defendant has the most money. A defendant who is only 5 percent at fault may end up paying 100 percent of a multimillion dollar judgment if every other defendant is insolvent.

This outcome is seen by supporters as an unfortunate but acceptable cost of protecting injured plaintiffs. Opponents argue it creates fundamentally unfair results and discourages participation in economic activity for fear of disproportionate liability exposure.

This debate has driven many states to reform or eliminate the doctrine over the past four decades.

How Do Defendants Recover Money From Each Other Through Contribution?

The Right of Contribution

When one defendant pays more than their proportionate share of a judgment under joint and several liability, they do not simply absorb the excess. They have a legal right to seek reimbursement from their co-defendants through a claim for contribution.

A defendant who pays more than their share can seek reimbursement from co-defendants through a contribution claim. This right exists under both common law principles and, in many states, specific contribution statutes.

How Contribution Claims Work in Practice

Contribution claims arise after a judgment has been paid. If Defendant A pays $600,000 of a $900,000 judgment, but their assigned fault percentage was only 20 percent, they have effectively paid $420,000 more than their share. They may then sue Defendants B and C to recover the amount each of them owed based on their respective fault percentages.

Some states allow defendants to bring contribution claims within the original lawsuit itself, through cross-claims or third party practice. Others require defendants to bring a separate action after the original judgment is satisfied. Practitioners must know which rule applies in their jurisdiction.

Indemnity Claims: A Related but Distinct Right

Indemnity is different from contribution. Contribution involves defendants dividing a loss proportionally. Indemnity involves one defendant being entirely reimbursed by another based on a prior agreement, a special legal relationship, or a finding that the other party was primarily responsible.

Contractual indemnity agreements are common in construction, real estate, and product distribution. A general contractor, for example, may require subcontractors to indemnify them for claims arising from the subcontractor’s work.

When joint and several liability results in the contractor paying a judgment, the indemnity clause gives them a direct claim against the subcontractor for full reimbursement.

Real Litigation Flow After a Joint Judgment

The full litigation timeline in a multi-defendant case typically unfolds in several stages.

- First, the plaintiff sues all defendants and obtains a joint and several judgment.

- Secondly, the plaintiff collects from the most accessible defendant.

- Thirdly, that paying defendant pursues contribution or indemnity claims against the others.

- An then the courts in the contribution proceeding may reapportion the loss based on the same fault percentages established at the original trial.

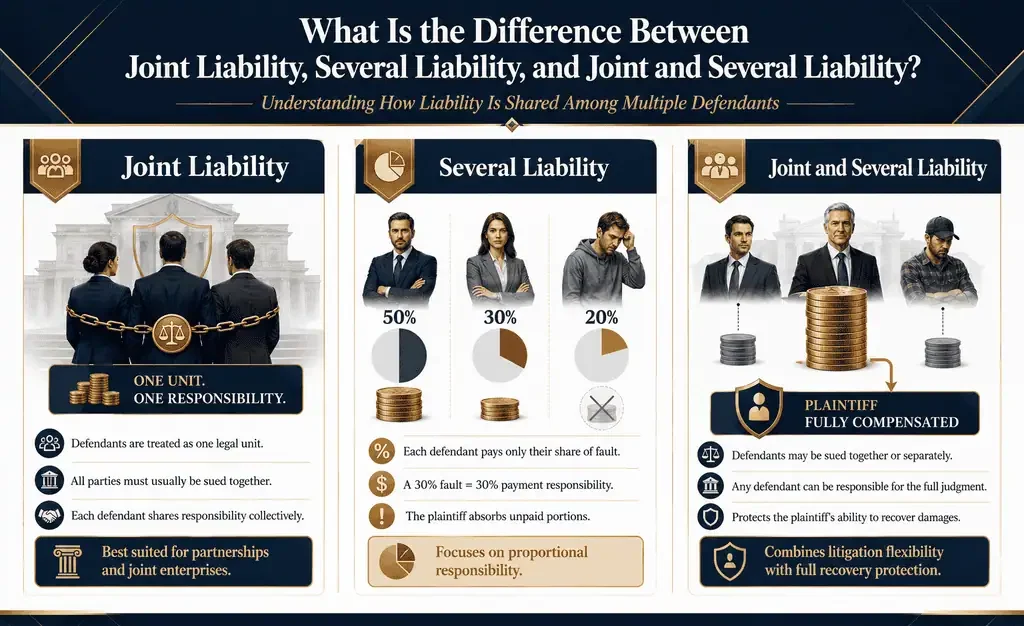

What Is the Difference Between Joint Liability, Several Liability, and Joint and Several Liability?

Joint Liability

Under pure joint liability, all defendants must be sued together and are collectively responsible for the judgment.

If one defendant is absent from the lawsuit, the court typically cannot enter a complete judgment. Joint liability most commonly applies to formal partnerships and joint enterprises where the parties have legally merged their activities.

Joint liability requires defendants to be sued together and treated as a single legal unit for purposes of the judgment.

Several Liability

Several liability, also called proportionate liability, limits each defendant’s obligation to their specific percentage of fault. A defendant found 30 percent at fault pays 30 percent of damages and nothing more. If other defendants cannot pay their shares, the plaintiff bears the loss.

Several liability limits each defendant’s payment to their own fault percentage. The plaintiff absorbs any shortfall caused by insolvent co-defendants.

Several liability is the preferred rule among defendant-side advocates and the direction in which many state legislatures have moved since the tort reform movement of the 1980s.

Joint and Several Liability

Joint and several liability merges both concepts. Defendants may be sued separately or together (the several aspect), but each defendant remains responsible for the full judgment regardless of their individual fault percentage (the joint aspect). This gives plaintiffs flexibility in both litigation strategy and collection.

Joint and several liability allows full recovery from one party. The plaintiff can pursue any of the multiple defendants for the complete judgment, combining the flexibility of several litigation with the protection of joint payment responsibility.

Why the Distinction Matters

The difference between these three systems is not merely academic. In a case involving $5 million in damages and three defendants with fault percentages of 60, 30, and 10 percent, the outcomes under each system are strikingly different.

- Under joint liability, all three must participate in the judgment and each shares collective responsibility.

- Under several liability, the plaintiff can only recover $3 million from Defendant A, $1.5 million from Defendant B, and $500,000 from Defendant C, with no cross-recovery if any defendant is broke.

- Under joint and several liability, the plaintiff can demand the full $5 million from Defendant A alone, leaving Defendant A to pursue Defendants B and C for their shares.

Which States Still Apply Joint and Several Liability and Which Limit It?

The landscape of joint and several liability in the United States is fragmented. Following decades of tort reform legislation, no single nationwide rule exists.

States fall into several broad categories, each with important nuances that practitioners must know.

States That Retain Pure Joint and Several Liability

A shrinking group of states maintain the traditional common law rule under which joint and several liability applies without significant fault-based limitations. In these jurisdictions, a plaintiff may recover the entire judgment from any one defendant regardless of that defendant’s percentage of fault.

- Delaware: Retains joint and several liability broadly in common law tort actions, including personal injury and wrongful death cases.

- Maine: Applies joint and several liability in most tort contexts, with limited statutory exceptions for specific categories of defendants.

- Maryland: Follows the traditional rule in personal injury cases, though courts have applied proportionality in limited circumstances.

- Massachusetts: Maintains joint and several liability in tort actions generally, with some legislative modifications in specific practice areas.

- Rhode Island: Applies joint and several liability under its comparative negligence framework, protecting plaintiffs from shortfalls.

- Vermont: Retains the rule broadly, with contribution rights available post-judgment.

- Virginia: Applies joint and several liability as a baseline rule in negligence cases involving multiple tortfeasors.

- Washington D.C.: Follows joint and several liability in personal injury litigation consistent with traditional common law principles.

States With Modified Joint and Several Liability

The largest group of states applies joint and several liability conditionally, typically based on the defendant’s percentage of fault. These hybrid systems attempt to balance plaintiff protection with proportionate defendant responsibility.

Threshold-Based Systems

Several states apply joint and several liability only when a defendant’s fault exceeds a specified threshold:

- Florida: Under current law, joint and several liability was largely abolished in 2006. Defendants are liable only for their proportionate share except in specific circumstances such as intentional torts, pollution, or situations where the defendant acted with conscious disregard for the safety of others.

- Hawaii: Applies joint and several liability only to defendants found more than 25 percent at fault. Below that threshold, the defendant is severally liable only for their proportionate share except for intentional tort

- New York: Uses a modified approach. Under New York‘s pure comparative fault system, joint and several liability applies to non-economic damages (pain and suffering) only when a defendant’s fault exceeds 50 percent. Economic damages remain subject to joint and several liability regardless of fault percentage. This distinction is critically important in high-value personal injury litigation.

- Ohio: Applies several liability as the general rule but imposes joint and several liability on defendants whose fault exceeds 50 percent.

- Utah: Limits joint and several liability to defendants with fault at or above 15 percent of total fault.

Category-Based Systems

Some states apply joint and several liability only in specific categories of cases or for specific categories of harm:

- California: Under Proposition 51 (1986), joint and several liability was retained for economic damages (medical expenses, lost wages) but eliminated for non-economic damages (pain and suffering, emotional distress). Each defendant pays only their proportionate share of non-economic damages. This split remains one of the most significant tort reform changes in any state.

- Illinois: Applies joint and several liability when the plaintiff is not at fault. If the plaintiff bears any fault, defendants are severally liable for their proportionate share, though exceptions exist for pollution and hazardous waste cases.

- Texas: Abolished joint and several liability for most defendants in 1995, retaining it only for defendants found more than 51 percent responsible, for defendants acting in concert, or for defendants committing intentional or criminal acts.

- Wisconsin: Applies joint and several liability for economic losses but not for non-economic losses when the plaintiff is partially at fault.

States That Have Largely Abolished Joint and Several Liability

A significant number of states have moved to pure several liability systems, where each defendant pays only their proportionate share of fault:

- Alaska: Converted to several liability for most tort cases, with exceptions for intentional conduct and certain environmental claims.

- Colorado: Applies several liability as the default rule following its 1986 tort reform legislation, limiting joint liability to intentional tortfeasors and those acting in concert.

- Georgia: Applies proportionate share liability under its apportionment statutes, with joint liability retained for parties acting in concert.

- Indiana: Each defendant is liable only for their own percentage of fault, with limited exceptions.

- Kansas: Abolished joint and several liability except for defendants acting in concert or performing hazardous activities.

- Michigan: Moved to several liability for non-economic damages, with joint liability retained for economic damages depending on the defendant’s fault percentage.

- Minnesota: Applies several liability in most cases, with joint and several retained when fault exceeds 15 percent in specific categories.

- Montana: Applies proportionate fault rules with very limited joint and several liability provisions.

- Nevada: Eliminated joint and several liability for non-economic damages and adopted pure proportionate liability following tort reform.

- North Dakota: Applies several liability, holding each defendant only for their proportionate share.

- Oklahoma: Adopted proportionate fault liability, limiting joint and several liability to parties acting in concert.

- Oregon: Applies several liability as the general rule for economic and non-economic damages, with exceptions for certain environmental and product liability cases.

A Note on Ongoing Legislative Change

The state-by-state rules described above reflect general principles as they existed through 2025. State legislatures continue to amend tort statutes regularly, and court decisions can significantly affect how statutes are interpreted and applied. Attorneys and litigants should always research the most current statutory text and case law in the relevant jurisdiction before relying on any general summary.

How Does Joint and Several Liability Interact With Comparative Fault Rules?

One of the most technically demanding aspects of joint and several liability is its interaction with comparative fault systems. Nearly every state has adopted some form of comparative fault, which means courts must consider how both systems apply simultaneously in a multi-defendant personal injury case.

Pure Comparative Fault States

In pure comparative fault states such as California, New York, Florida, and Alaska, a plaintiff may recover damages even if they are 99 percent at fault, but their damages are reduced by their own fault percentage. When joint and several liability also applies, the court first calculates total damages and then reduces that amount by the plaintiff’s percentage of fault before applying joint and several liability against the defendants.

For example: A plaintiff is found 20 percent at fault. The jury awards $1,000,000 in total damages. The plaintiff’s recovery is reduced to $800,000 by their 20 percent fault. Under joint and several liability, the plaintiff may collect the full $800,000 from any one of the defendants.

Modified Comparative Fault States

Most states use modified comparative fault systems, which bar recovery if the plaintiff’s fault exceeds a specified threshold, typically either 50 or 51 percent. In these states, the plaintiff must first survive the fault bar before joint and several liability becomes relevant.

In a 50 percent bar state, a plaintiff found 51 percent at fault recovers nothing. A plaintiff found 49 percent at fault has their damages reduced by 49 percent, and joint and several liability (if available in that state) applies to the remaining recoverable amount.

The Complexity of Allocating Plaintiff Fault

Courts must determine whether the plaintiff’s comparative fault affects only the total damages calculation or also affects how defendants are allocated responsibility among themselves. In most jurisdictions, the plaintiff’s fault percentage reduces the total award, and the defendants then share responsibility for the reduced amount according to their own fault allocations.

This can create significant tactical decisions for plaintiff’s attorneys regarding how aggressively to address the plaintiff’s own conduct, particularly in states where the fault bar creates an all-or-nothing threshold.

What Are Real World Examples of Joint and Several Liability Cases?

Multi Vehicle Car Accidents

Multi-vehicle accidents are one of the most common contexts for joint and several liability claims. Consider a scenario where three drivers all engage in aggressive behavior on a highway, leading to a chain reaction collision that seriously injures a fourth driver.

If the jury finds the three aggressive drivers each contributed to the accident and that their fault is indivisible because it is impossible to say which driver’s action directly caused the final impact, joint and several liability allows the injured plaintiff to collect the full judgment from any one of them. The plaintiff’s attorney will likely focus on whichever driver has the highest liability insurance limits.

Toxic Tort and Asbestos Exposure Cases

Joint and several liability is used in cases where harm cannot be divided among defendants, such as toxic exposure claims. These cases represent the doctrine at its most complex and financially significant.

Asbestos litigation has produced some of the largest applications of joint and several liability in American legal history. Workers exposed to asbestos over the course of a career often worked at multiple sites, used products from dozens of manufacturers, and breathed air contaminated by several employers simultaneously.

When mesothelioma or other asbestos-related diseases develop decades later, courts cannot determine which manufacturer or employer’s asbestos caused the specific cellular damage that led to cancer. The injury is indivisible, and joint and several liability has historically allowed plaintiffs to recover from any solvent defendant in the chain, even when dozens of other defendants have already filed for bankruptcy.

Medical Malpractice Involving Multiple Providers

Medical malpractice cases frequently involve multiple healthcare providers whose overlapping negligence contributes to a single patient injury. A surgeon, anesthesiologist, and nursing staff may each make errors during a single procedure that together cause a catastrophic outcome such as brain damage or wrongful death.

When each provider’s error is impossible to separate from the others in terms of causation, joint and several liability allows the patient or their estate to pursue full recovery from any one provider. Hospitals, in particular, can face joint liability for the combined negligence of multiple employed providers even when each individual deviation was relatively minor.

Product Liability Cases

Product liability cases involving multiple defendants in the distribution chain are another fertile ground for joint and several liability. When a defective product causes injury, the manufacturer, distributor, and retailer may all be named as defendants.

If a component manufactured by one company, assembled by a second, distributed by a third, and sold by a fourth causes an explosion that injures a consumer, and if the defect resulted from collective failures at multiple stages, joint and several liability allows the injured consumer to collect the full judgment from the party with the deepest pockets, typically the manufacturer or the major retailer.

What Are the Advantages and Criticisms of Joint and Several Liability?

Advantages for Injured Plaintiffs

The primary benefit of joint and several liability is full compensation for plaintiffs in cases involving multiple defendants. The rule ensures that an injured person is not left with a partial recovery simply because some of those responsible lack assets or insurance.

- Plaintiffs do not bear the financial risk of insolvent defendants.

- Recovery is not delayed or reduced by complex allocation disputes among defendants.

- The rule incentivizes defendants to settle early to avoid disproportionate exposure.

- It reinforces the deterrent function of tort law by ensuring that all contributors to harm are accountable for full consequences.

Risks and Criticisms From the Defendant Perspective

A minimally responsible defendant can end up paying the full judgment if others cannot pay. This outcome is widely cited as the central unfairness of joint and several liability from a defendant’s perspective.

The criticism is most acute when a defendant with minimal fault, say 5 percent, is forced to pay 100 percent of a large judgment because co-defendants are bankrupt. That defendant then has a contribution claim against those insolvent parties that may be practically worthless.

- Small businesses and individuals can face catastrophic financial exposure for relatively minor roles in causing harm.

- The rule may deter participation in legitimate commercial activities out of fear of disproportionate liability.

- Deep-pocket targeting can distort litigation incentives, turning suits into financial recovery exercises rather than fault-based accountability.

- Defendants who are primarily responsible may strategically arrange their finances to be judgment-proof, knowing that a solvent co-defendant will absorb the loss.

The Legal Fairness Debate

The tension between plaintiff protection and defendant proportionality has fueled the tort reform debate in American law for over four decades.

Plaintiff advocates argue that the rule correctly places the financial risk of insolvent defendants on those who created the dangerous condition rather than on the innocent victim. Defendant advocates argue that proportionate liability is the more just system because financial responsibility should match actual fault.

Neither side has conclusively won the argument. The continued patchwork of state approaches reflects an ongoing societal negotiation about the proper balance between these competing values.

Frequently Asked Questions About Joint and Several Liability

Can you sue one defendant for full damages even if others are also at fault?

Yes. In states that follow joint and several liability, a plaintiff may file suit against only one defendant and seek the full judgment amount from that party alone, even if other parties also contributed to the harm. The plaintiff is not required to include all responsible parties in the lawsuit, though tactical and strategic reasons often make it advantageous to do so.

What happens if one defendant cannot pay their share of the judgment?

In joint and several liability states, if one defendant is insolvent, the plaintiff may collect the entire remaining balance from any solvent co-defendant. That solvent defendant then has a contribution claim against the insolvent party, though collecting on it may be difficult or impossible. This is one of the core functions of the doctrine: protecting plaintiffs from a co-defendant’s financial inability to pay.

Can liability be divided between defendants after one pays the full judgment?

Yes. After one defendant satisfies a joint and several judgment, they may bring a contribution claim against co-defendants to recover the amount those defendants should have paid based on their fault percentages. Courts will allocate the loss according to the fault percentages established in the original trial unless the parties agree to different terms.

Do all states follow joint and several liability?

No. The United States does not have a uniform rule. Some states apply full joint and several liability. Others apply it only when a defendant’s fault exceeds a threshold percentage. Several states have abolished it entirely and replaced it with proportionate several liability. The applicable rule depends entirely on the state where the lawsuit is filed.

How does insurance affect joint and several liability?

Insurance plays a critical practical role. A defendant’s liability insurer pays up to the policy limits on the defendant’s behalf. If a joint and several judgment exceeds the policy limits of the targeted defendant, that defendant becomes personally responsible for the excess. Plaintiffs and their attorneys routinely investigate all defendants’ insurance coverage early in litigation to identify the best targets for collection.

What is the difference between joint and several liability and proportionate liability?

Joint and several liability allows a plaintiff to collect the full judgment from any single defendant. Proportionate liability, also called several liability, limits each defendant to paying only their assigned fault percentage. The choice between these systems has enormous financial consequences in cases involving high damages and defendants with varying levels of solvency.

Can a plaintiff with comparative fault still benefit from joint and several liability?

Yes, in many states. The plaintiff’s own fault reduces the total damages award, but once that reduction is applied, the remaining damages may still be subject to joint and several liability against the defendants. A plaintiff who is 30 percent at fault and is awarded $1,000,000 in total damages would have their recovery reduced to $700,000, but could still collect that full $700,000 from any one defendant in a joint and several liability jurisdiction.

Are there situations where joint and several liability does not apply even in states that generally follow it?

Yes. Many states that follow the doctrine have carved out exceptions. Defendants whose fault falls below a statutory threshold may be subject to several liability only. Certain categories of defendants, such as government entities or healthcare providers, may have statutory limitations. Intentional tortfeasors may sometimes face different rules than negligent ones. Practitioners must examine both the general rule and any applicable exceptions in every case.

What is tortfeasor liability and how does it connect to joint and several liability?

A tortfeasor is any party whose wrongful conduct causes injury or damage to another. Tortfeasor liability refers broadly to the legal obligations that arise from that wrongful conduct. In multi-party cases, co-tortfeasors are the multiple defendants whose combined or overlapping conduct caused a single harm. Joint and several liability is the specific rule that governs how co-tortfeasors are held accountable to the plaintiff.

How has the tort reform movement affected joint and several liability nationally?

Beginning in the 1970s and accelerating through the 1980s and 1990s, tort reform advocates successfully lobbied state legislatures to limit or abolish joint and several liability. The American Tort Reform Association and similar organizations argued that the rule created excessive liability for businesses, distorted insurance markets, and produced unfair outcomes for minimally responsible defendants. As a result, a majority of states have now modified or eliminated the traditional rule, with only a minority retaining it in its pure common law form.